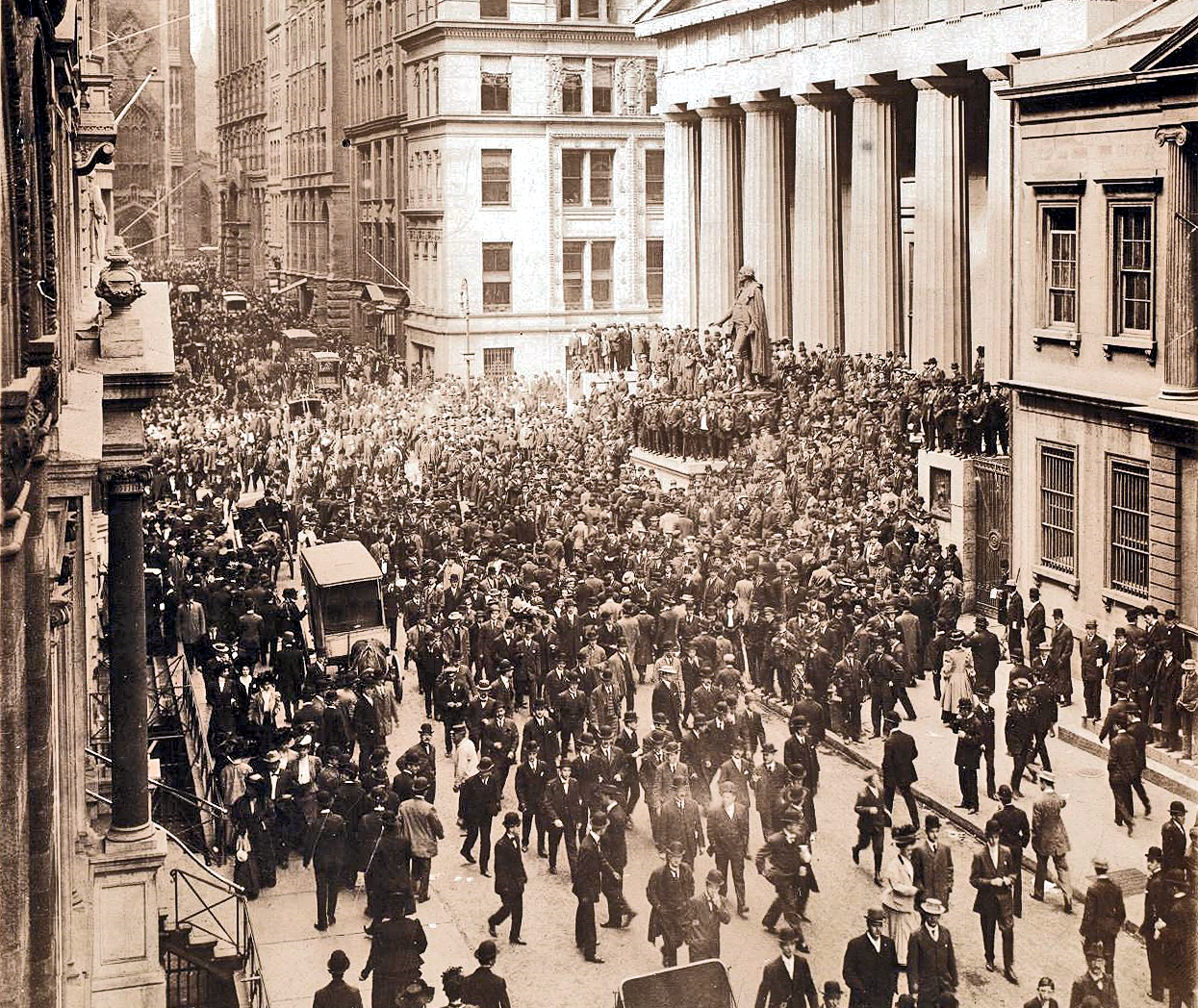

Pre-Federal Reserve Banking Instability in New York (1791, 1913)

The financial history of the United States between 1791 and 1913 centers on the volatile concentration of capital in New York City. Before the Federal Reserve Act of 1913 established a decentralized central banking system, New York acted as the nation's de facto lender of last resort. This arrangement proved disastrously unstable. The absence of a public central bank meant that the liquidity of the entire American economy rested on a fragile network of private commercial banks in Manhattan. These institutions operated under a structural flaw known as reserve pyramiding. This method funneled the cash reserves of rural and regional banks into the vaults of New York City banks, which then lent those funds to stock market speculators.

Alexander Hamilton founded the Bank of New York in 1784 to bring order to the post-Revolutionary financial chaos. The federal government later attempted to stabilize the currency through the Bank of the United States (1791, 1811) and the Second Bank of the United States (1816, 1836). Both institutions maintained their headquarters in Philadelphia yet managed significant operations in New York. When political opposition allowed their charters to expire, the nation entered the "Free Banking Era." New York passed the Free Banking Act of 1838. This legislation allowed any group meeting minimum capital requirements to open a bank. The result was an explosion of state-chartered institutions issuing their own banknotes. These notes frequently traded at discounts relative to their face value. The absence of a unified currency created friction in commerce and uncertainty in credit markets.

The Civil War necessitated a more regulated system to finance the Union war effort. The National Banking Acts of 1863 and 1864 established a system of nationally chartered banks and a uniform currency backed by U. S. government bonds. This legislation inadvertently codified the instability of the New York market. The law New York City as a "Central Reserve City." National banks in the interior of the country, known as "country banks," were required to hold 15% reserves against their deposits. The law permitted these country banks to keep three-fifths of their required reserves as interest-bearing deposits in New York City national banks. New York banks, in turn, were required to hold a 25% reserve in specie or lawful money.

New York banks competed aggressively for these interior deposits by offering attractive interest rates. To generate the returns necessary to pay this interest, Wall Street banks lent the deposited funds into the call loan market. Call loans were demand loans used by stockbrokers to finance the purchase of securities on margin. This created a direct and dangerous link between the nation's banking reserves and the volatility of the stock market. The system functioned adequately during calm periods. It failed catastrophically during the autumn harvest. Every fall, farmers in the Midwest and South withdrew physical cash to pay for labor and transport crops. Country banks responded by drawing down their balances in New York. To meet these withdrawal requests, New York banks had to call in their loans to stockbrokers. Brokers then sold stocks to repay the loans. This selling pressure frequently triggered market crashes and banking panics.

| Panic Year | Trigger Event | NY Clearing House Action | Economic Consequence |

|---|---|---|---|

| 1873 | Failure of Jay Cooke & Co. (Railroad speculation) | Issued $26. 6 million in Loan Certificates | NYSE closed for 10 days; Long Depression begins |

| 1893 | Railroad failures; Gold reserve depletion | Issued $41. 5 million in Loan Certificates | 500+ banks failed; 18% unemployment |

| 1907 | Failed corner on United Copper; Knickerbocker Trust run | Issued $101 million in Loan Certificates | Call money rates hit 125%; Led to Federal Reserve Act |

The Panic of 1907 serves as the definitive example of this widespread failure. The emergency began outside the regulated national banking system, within the "shadow banking" sector of Trust Companies. Trust companies in New York operated under state charters that allowed them to hold lower cash reserves, frequently around 5%, compared to the 25% required for national banks. They also engaged in riskier investment activities. On October 16, 1907, a speculative attempt to corner the stock of the United Copper Company failed. The collapse entangled the Knickerbocker Trust Company, the third-largest trust in the city. On October 22, a run on the Knickerbocker began. Depositors withdrew $8 million in less than three hours. The institution suspended operations shortly after noon.

The contagion spread instantly. Regional banks, fearing a total collapse, accelerated their withdrawals of reserves from New York. The liquidity squeeze sent interest rates in the call money market skyrocketing. By October 24, the rate for overnight money on the New York Stock Exchange hit 125%. Brokers could not secure funds to hold their positions. The market faced total liquidation. In the absence of a central bank, J. P. Morgan organized a private rescue. He summoned the city's leading financiers to his library and coerced them into pledging $25 million to shore up the trust companies. The United States Treasury deposited $25 million into New York banks to add liquidity. Even with these interventions, the panic for weeks.

The New York Clearing House Association played a important insufficient role during these crises. Established in 1853 to settle accounts between city banks, the Clearing House functioned as a proto-central bank during emergencies. It issued "Clearing House Loan Certificates," which allowed member banks to settle balances with each other using collateral rather than cash. This preserved cash for payouts to panicked depositors. In 1907, the Clearing House issued over $100 million in these certificates. This method provided elasticity to the money supply within the closed loop of the Clearing House members. It could not, yet, print legal tender or provide unlimited liquidity to the broader economy.

The aftermath of 1907 exposed the inability of private bankers to manage the national money supply. The concentration of reserves in New York meant that a local speculative failure could freeze the commerce of the entire nation. The Pujo Committee of 1912 investigated the "Money Trust," revealing the immense power held by a small group of New York bankers. The investigation showed that J. P. Morgan and his associates held 341 directorships in 112 corporations with aggregate resources of $22 billion. This consolidation of power, combined with the widespread fragility demonstrated in 1907, forced the political consensus toward a public solution. The resulting Federal Reserve Act of 1913 sought to decentralize reserves and create an elastic currency, ending the era where the American economy lived and died by the daily call loan rates in Manhattan.

Establishment and the Benjamin Strong Directorate 1914, 1928

| Event | Date | Significance |

|---|---|---|

| New York Fed Opens | Nov 16, 1914 | Established with $20M capital; Benjamin Strong as Governor. |

| Liberty Loan Drives | 1917, 1919 | Shifted Fed focus from commercial paper to government debt. |

| Discovery of OMO | 1922, 1923 | Accidental realization that buying securities creates bank reserves. |

| Long Island Summit | July 1927 | Secret meeting leading to rate cuts that fueled the 1929 bubble. |

Following the war and the sharp recession of 1920, 1921, the New York Fed stumbled upon its most policy tool: Open Market Operations. In 1922, seeking to boost their own earnings during a period of low lending activity, district banks began purchasing government securities. Strong and his economists realized that these purchases did more than generate interest income; they injected reserves into the banking system, lowering interest rates and stimulating credit. Conversely, selling securities drained reserves. Recognizing the power of this lever, the System created the Open Market Investment Committee (OMIC) in 1923. Strong chaired this committee, centralizing national monetary policy within the walls of the New York Fed and bypassing the passive Board in Washington. Strong's tenure was also defined by his close alliance with Montagu Norman, the Governor of the Bank of England. The two men operated a private foreign policy, frequently communicating via cable and meeting in secret to coordinate transatlantic finance. Their primary objective was the restoration of the international gold standard, which had collapsed during the war. Britain returned to gold in 1925, the pound sterling remained overvalued and under pressure. To support the Bank of England, Strong kept U. S. interest rates artificially low, discouraging gold from flowing out of London and into New York vaults. This policy culminated in the secret central bank conference of July 1927. Strong hosted Montagu Norman, Hjalmar Schacht of the Reichsbank, and Charles Rist of the Bank of France at the Ogden Mills estate on Long Island. During this clandestine gathering, Strong agreed to cut the New York discount rate from 4 percent to 3. 5 percent. The move was intended to relieve pressure on the British pound, yet it had a catastrophic side effect at home. The cheap credit flooded into the New York Stock Exchange, fueling the speculative mania that would eventually crash the market. Critics later described this injection of liquidity as a "coup de whisky" for the stock market. Benjamin Strong died on October 16, 1928, following surgery for diverticulitis. His death left the Federal Reserve leaderless at a moment of extreme financial peril. The New York Fed had successfully centralized power, yet without Strong's forceful personality, the System paralyzed. The Board in Washington and the directors in New York spent the subsequent months in a deadlock, unable to agree on a method to curb the stock market speculation Strong's policies had helped ignite. The "headless" nature of the Fed in 1929 was a direct result of the institution being built around the singular authority of its Governor.

Construction of the 33 Liberty Street Fortress and Gold Vault

The construction of the Federal Reserve Bank of New York at 33 Liberty Street was not an architectural project; it was a psychological operation designed to project impregnable stability following decades of banking panics. In 1919, the bank's directors held a design competition, selecting the firm York and Sawyer. Their winning proposal rejected the modern skyscraper aesthetic in favor of a massive Florentine Renaissance, modeled directly on the Palazzo Strozzi and Palazzo Vecchio in Italy. The architects intended the rusticated limestone and sandstone façade, marked by deep horizontal and vertical grooves, to visually communicate that the institution was a citadel of permanent wealth, capable of withstanding any financial storm or physical assault.

Construction began in 1921 and concluded in 1924, with a total cost of approximately $18. 7 million, a sum equivalent to roughly $350 million in 2026 purchasing power. The engineering challenges were immense. To support the weight of the and the gold it would house, workers excavated down to the bedrock of Manhattan Island. This required digging 80 feet street level and 50 feet sea level. The foundation rests on 99 concrete piers poured directly onto the schist, ensuring the structure could bear the load of the world's largest concentration of monetary gold without settling.

The centerpiece of this subterranean is the gold vault, a three-story bunker engineered to be waterproof, airtight, and virtually impenetrable. Unlike typical bank vaults with swinging rectangular doors, the New York Fed's vault is secured by a 90-ton steel cylinder set within a 140-ton steel-and-concrete frame. To open the vault, the cylinder must rotate 90 degrees, aligning a narrow passageway with the entrance. When closed, the cylinder drops slightly to create a hermetic seal, protecting the contents from flooding, a necessary precaution given the vault's depth the water table. Security dictate that opening the vault requires a multi-person control group; no single individual holds the combination or authority to access the reserves.

Inside the vault, the gold is stored in 122 separate compartments, each assigned to a specific account holder. As of early 2026, the vault houses approximately 507, 000 gold bars, weighing roughly 6, 331 metric tons. This stockpile represents the largest known depository of monetary gold in the world, surpassing even the United States Bullion Depository at Fort Knox. Notably, the Federal Reserve Bank of New York owns none of this gold; approximately 98 percent is held in custody for the central banks of 36 foreign nations, the International Monetary Fund, and other international organizations. The bars are stacked on pallets, and the floor itself bears the scars and indentations of heavy gold bricks dropped by workers over the last century.

The building's interior reinforces the theme through the extensive use of wrought iron, crafted by master blacksmith Samuel Yellin. Yellin produced over 200 tons of decorative ironwork for the bank, including the massive lanterns flanking the main entrance and the intricate grilles protecting the teller windows. This commission remains the largest decorative wrought iron job ever completed in the United States. The sheer of the materials, steel, stone, and gold, serves the original 1919 mandate: to create a physical embodiment of the Federal Reserve's power that would endure as long as the bedrock it sits upon.

| Feature | Details |

|---|---|

| Construction Period | 1921, 1924 (Main Building); 1935 (Extension) |

| Architectural Style | Florentine Renaissance (Palazzo Strozzi influence) |

| Vault Depth | 80 feet street level; 50 feet sea level |

| Vault Door method | 90-ton rotating steel cylinder in 140-ton frame |

| Gold Holdings (2026) | ~507, 000 bars; ~6, 331 metric tons |

| Foundation | 99 concrete piers anchored to Manhattan bedrock |

| Total Cost (1924) | ~$18. 7 million (~$350 million adjusted for 2026) |

Liquidationist Policy and the Great Depression 1929, 1933

| Year | FRBNY Discount Rate (Peak) | M2 Money Supply Change | Bank Suspensions (National) |

|---|---|---|---|

| 1929 | 6. 0% | -0. 1% | 659 |

| 1930 | 3. 0% | -3. 1% | 1, 350 |

| 1931 | 3. 5% | -7. 1% | 2, 293 |

| 1932 | 3. 0% | -15. 5% | 1, 453 |

| 1933 | 3. 5% | -11. 2% (Jan-Mar) | 4, 000+ |

The contraction of the money supply was not a natural phenomenon a direct result of policy choices. Between 1929 and 1933, the quantity of money in the United States fell by one-third. This deflationary spiral made debt repayment impossible for farmers and businesses. As prices fell, the real value of debt rose. Borrowers defaulted, causing more bank failures, which destroyed more money, leading to further price declines. The Federal Reserve had the power to arrest this pattern by aggressively purchasing government bonds and expanding the monetary base. It refused to do so. By the winter of 1932, the banking system had ceased to function. Governors in states like Nevada and Michigan began declaring statewide banking holidays to prevent total liquidation. The Federal Reserve Bank of New York, once the bulwark of the system, watched helplessly as the panic reached Manhattan. On the morning of March 4, 1933, the day of Franklin D. Roosevelt's inauguration, Governor Herbert Lehman of New York declared a bank holiday. The financial capital of the world closed for business. The Federal Reserve System had failed in its primary mission. It had not only failed to prevent a panic. It had engineered the conditions that made the collapse absolute. The liquidationist experiment had succeeded in purging the economy of speculation, it had nearly destroyed the capitalist system in the process.

Bretton Woods Implementation and Foreign Exchange Operations

| Era | Primary method | Strategic Objective | Operational Peak/Status |

|---|---|---|---|

| 1962, 1971 | Reciprocal Currency Arrangements | Defend $35/oz gold peg; hide US deficits. | $11. 7 billion in total lines (1971). |

| 1985, 1995 | Directional Intervention (Spot/Forward) | Devalue USD (Plaza Accord); stabilize rates (Louvre). | Aggressive selling of USD vs. DEM/JPY. |

| 2007, 2010 | Liquidity Swap Lines (Temporary) | Prevent global banking collapse due to dollar absence. | $580 billion outstanding (Dec 2008). |

| 2020, Present | Standing Liquidity Swaps & FIMA Repo | Backstop global sovereign dollar demand. | $450 billion (May 2020); Standing status (2026). |

September 11 Attacks and Payment System Continuity

| Metric | Pre-Attack Average (2001) | emergency Peak (Sept 12, 14, 2001) | Increase Factor |

|---|---|---|---|

| Discount Window Lending | $200 Million | $45. 5 Billion | 227x |

| Daily Check Float | $766 Million | $47. 4 Billion | 61x |

| Open Market Operations (Repos) | $2-5 Billion | $81. 25 Billion | ~20x |

| Swap Lines (ECB) | $0 | $50 Billion (Authorized) | N/A |

A second, less visible emergency unfolded in the physical check clearing system. In 2001, of American commerce still relied on paper checks, which the Federal Reserve transported across the country via a fleet of cargo planes. When the Federal Aviation Administration grounded all civil aircraft, millions of checks became stranded at airports. The Federal Reserve operates on a "availability schedule," meaning it credits the bank depositing a check before it actually collects the funds from the bank that wrote the check. The gap between these two events is called "float." With planes grounded, the Fed could not present checks for payment, yet it continued to credit the accounts of depositing banks to maintain economic stability. This decision caused the daily float to swell from a standard $766 million to a $47. 4 billion on September 13. In effect, the Federal Reserve provided an interest-free loan of nearly $50 billion to the banking sector simply by honoring the availability schedule of stranded paper checks. This specific logistical failure accelerated the push for the Check Clearing for the 21st Century Act (Check 21), which was signed into law in 2003 to allow for electronic check substitution. The FRBNY also had to manage the global demand for U. S. dollars. Foreign banks, unable to settle transactions in New York, faced a dollar absence. To address this, the Federal Reserve established temporary swap lines with the European Central Bank ($50 billion) and the Bank of England ($30 billion). These agreements allowed foreign central banks to exchange their currencies for dollars, which they then lent to institutions in their jurisdictions. This action prevented the liquidity emergency in Lower Manhattan from triggering a credit freeze in London and Frankfurt. Operational continuity at 33 Liberty Street required extraordinary measures. The building's air intake systems were sealed to prevent the infiltration of dust and smoke from the smoldering wreckage nearby. Staff slept in the bank's offices, managing the extended operating hours of Fedwire, which remained open until late into the night to allow banks to reconcile their chaotic ledgers. The FRBNY waived fees for "daylight overdrafts", the negative balances banks run during the day, further encouraging institutions to keep payments moving without fear of penalty. The legacy of September 11 for the Federal Reserve Bank of New York was a fundamental restructuring of financial redundancy. Before 2001, "backup" frequently meant a data center in the same city. The attacks demonstrated that geographic concentration was a single point of failure. In the years that followed, the Fed and major clearing banks moved serious operations to dispersed locations, ensuring that a physical catastrophe in Manhattan could never again hold the U. S. payment system hostage. The emergency proved that the central bank's power lies not just in setting interest rates, in its ability to physically and digitally force liquidity through a paralyzed system.

Maiden Lane Vehicles and the 2008 AIG Intervention

The following table details the payments made to major counterparties under the Maiden Lane III facility, retiring the CDS contracts at face value:

| Counterparty | Payment Amount (Approx. $ Billions) | Domicile |

|---|---|---|

| Goldman Sachs | $12. 9 | United States |

| Société Générale | $11. 9 | France |

| Deutsche Bank | $11. 8 | Germany |

| Barclays | $8. 5 | United Kingdom |

| Merrill Lynch | $6. 8 | United States |

| Bank of America | $5. 2 | United States |

| UBS | $5. 0 | Switzerland |

FRBNY officials defended the decision to pay par, arguing that they absence the legal use to force haircuts and that a selective default would have triggered a widespread collapse. Geithner and his team contended that negotiating discounts would have taken too much time and might have prompted the counterparties to declare AIG in default, causing a chaotic bankruptcy. Yet, the SIGTARP report disputed this narrative, noting that one counterparty, UBS, had initially offered to take a haircut, a concession the FRBNY did not pursue with other banks. The refusal to use the Fed's status as a regulator to demand concessions from the bank beneficiaries remains a central point of historical criticism. The FRBNY also attempted to keep the identities of these counterparties secret. It was only after sustained pressure from Congress and a subpoena from the House Oversight Committee that the details of the Maiden Lane III payments were released in March 2009. The that billions of dollars in Federal Reserve aid had flowed directly to foreign banks and solvent domestic competitors like Goldman Sachs fueled public outrage and legislative scrutiny over the transparency of the Fed's emergency lending powers under Section 13(3). Financially, the Maiden Lane vehicles eventually recovered their costs. As the markets stabilized in the years following the emergency, the value of the RMBS and CDO assets held in the SPVs rebounded. The FRBNY managed these portfolios carefully, selling assets gradually to avoid flooding the market. Maiden Lane II repaid its loan to the New York Fed in full by February 2012, generating a net gain of approximately $2. 8 billion. Maiden Lane III repaid its loan in June 2012, resulting in a net gain of approximately $6. 6 billion for the Fed. While these profits are frequently to justify the intervention, they do not negate the massive risk transfer that occurred in 2008, nor do they address the moral hazard established by insulating private counterparties from the consequences of their own risk management failures. The Maiden Lane interventions demonstrated the FRBNY's capacity to act as a "market maker of last resort," purchasing distressed assets directly to prevent a fire sale, a significant expansion of its traditional role as a lender of last resort.

Quantitative Easing and Asset Purchase Mechanics 2009, 2014

Between 2009 and 2014, the Federal Reserve Bank of New York (FRBNY) fundamentally altered the mechanics of American monetary policy, shifting from targeting the price of money (interest rates) to manipulating the quantity of money (reserves). This period marked the operationalization of Large- Asset Purchases (LSAP), commonly known as Quantitative Easing (QE). Unlike the discount window lending of the 1913 era or the modest open market operations of the 1990s, the FRBNY's Open Market Trading Desk (the Desk) began absorbing trillions of dollars in securities directly from the secondary market. This action exploded the Federal Reserve's balance sheet from approximately $900 billion in late 2008 to $4. 5 trillion by October 2014. The Desk executed these trades not through open outcry or telephone banks, via FedTrade, a proprietary electronic auction system that connected the New York Fed directly to its network of Primary Dealers.

The phase, QE1, began in earnest following the November 2008 announcement accelerated through 2009. The Federal Open Market Committee (FOMC) directed the New York Fed to purchase $1. 25 trillion in Mortgage-Backed Securities (MBS) guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae, alongside $175 billion in agency debt and $300 billion in long-term Treasury securities. This was a radical departure from the Fed's history; for the time since the central bank's inception, the FRBNY was not managing liquidity actively allocating credit to a specific sector, housing. The Desk executed these purchases by soliciting competitive offers from dealers such as Goldman Sachs, J. P. Morgan, and others, accepting the most attractive prices to minimize cost while meeting volume. By the conclusion of QE1 in March 2010, the FRBNY held nearly one-sixth of the entire U. S. mortgage market, a concentration of financial power unknown even during the panic of 1907.

Following a brief pause, the recovery faltered, leading to QE2 in November 2010. This program reverted to the Fed's traditional asset class, U. S. Treasuries, at a volume that historical norms. The Desk purchased $600 billion in longer-term Treasury securities at a pace of roughly $75 billion per month. The operational goal was the "portfolio balance channel." By removing safe, long-duration assets from the market, the FRBNY forced private investors to rebalance their portfolios into riskier assets like corporate bonds and equities, theoretically lowering yields and stimulating investment. Critics argued this method distorted price discovery, yet the Desk continued its aggressive acquisition schedule through June 2011.

In September 2011, the FRBNY implemented the Maturity Extension Program (MEP), colloquially dubbed "Operation Twist." Unlike QE, this maneuver did not expand the balance sheet. Instead, the Desk sold $667 billion -term Treasury securities (maturing in 3 years or less) and used the proceeds to buy an equivalent amount of long-term securities (6 to 30 years). This operation flattened the yield curve, driving down long-term borrowing costs without creating new reserves. The logistical complexity was high; the Desk simultaneously managed massive sell-orders and buy-orders, reshaping the maturity profile of the System Open Market Account (SOMA) in real-time. This echoed a smaller, less successful attempt at a similar "twist" operation in 1961, though the 2011 iteration involved sums adjusted for inflation that dwarfed the Kennedy-era experiment.

The final and most aggressive phase, QE3, launched in September 2012. Unlike its predecessors, QE3 was open-ended, with no fixed expiration date or total dollar cap. The Desk initially purchased $40 billion in agency MBS per month. In December 2012, this increased to include $45 billion in Treasury securities monthly, bringing the total flow to $85 billion every month. This "infinity QE" continued until the economy showed tangible improvement. The sheer volume of transactions required the FRBNY to dominate the Treasury market, frequently purchasing a significant percentage of the available inventory in specific CUSIPs. The program continued at full velocity until December 2013, when the Desk began "tapering" purchases, reducing the monthly buy volume by $10 billion at each successive meeting until the program concluded in October 2014.

| Program | Operational Dates | Primary Assets Purchased | Approximate Total Size |

|---|---|---|---|

| QE1 | Nov 2008 , Mar 2010 | Agency MBS, Agency Debt, Treasuries | $1. 725 Trillion |

| QE2 | Nov 2010 , Jun 2011 | Long-term Treasuries | $600 Billion |

| Operation Twist (MEP) | Sep 2011 , Dec 2012 | Long-term Treasuries (funded by short-term sales) | $667 Billion (Neutral Impact) |

| QE3 | Sep 2012 , Oct 2014 | Agency MBS, Long-term Treasuries | $1. 6 Trillion (Cumulative) |

The mechanics of these purchases relied heavily on the Primary Dealer system. These banks acted as the exclusive counterparties for the FRBNY. When the Desk announced an operation, dealers submitted offers via FedTrade within a specified time window, frequently as short as 45 minutes. The system's algorithms ranked offers to ensure the Fed paid the lowest possible price for the required securities. Settlement occurred on a T+1 basis, with the Fed crediting the dealer's reserve account. This process created "excess reserves" in the banking system, which grew from negligible levels in 2007 to over $2. 5 trillion by 2014. These reserves did not immediately enter the broader economy as circulating currency remained on bank balance sheets, earning interest paid by the Fed, a policy tool introduced in 2008 that fundamentally changed the profit incentives for depository institutions.

By the end of 2014, the FRBNY had nationalized of the U. S. duration risk. The central bank held approximately 25% of all outstanding Treasury securities and over 30% of the agency MBS market. This concentration raised serious questions about market liquidity and the ability of private actors to function without the "Fed put." While the 1790s saw Alexander Hamilton use the Bank of the United States to stabilize credit, and the 1930s saw the Fed fail to provide adequate liquidity, the 2009, 2014 era represented the total inversion of the central bank's role: rather than the lender of last resort, the New York Fed became the buyer of resort, permanently altering the pricing structure of global financial assets.

The Carmen Segarra Tapes and Supervisory Irregularities

In the aftermath of the 2008 financial collapse, the Federal Reserve Bank of New York faced a emergency of competence and credibility. To diagnose its internal failures, President William Dudley commissioned a secret report in 2009 from Columbia University professor David Beim. The resulting document, known as the Beim Report, delivered a scathing indictment of the New York Fed's culture. Beim found an organization crippled by a "culture of consensus" where examiners were discouraged from raising objections that might delay bank operations. The report explicitly identified a form of "regulatory capture," noting that supervisors paid excessive deference to the banks they were charged with regulating. To correct this, Beim recommended the Fed hire specialized, expert examiners who would possess the confidence and experience to challenge the most financial institutions on Wall Street.

Carmen Segarra was hired in October 2011 as part of this new initiative. A Cornell-educated lawyer with over a decade of experience in compliance, she was assigned to the onsite team at Goldman Sachs. Her mandate was to examine the bank's legal and compliance risks. Segarra arrived at a moment when Goldman Sachs faced scrutiny for its role in a massive energy sector transaction: the $21 billion acquisition of El Paso Corporation by Kinder Morgan. The deal was with conflicts of interest. Goldman Sachs acted as the advisor to El Paso, yet the bank also held a $4 billion stake in Kinder Morgan and controlled two seats on its board. also, the lead Goldman banker advising El Paso personally owned approximately $340, 000 in Kinder Morgan stock. In Delaware, Chancellor Leo Strine later criticized the arrangement, stating that Goldman's involvement was "tainted" by these conflicts.

Segarra began her examination by requesting Goldman Sachs' firm-wide conflict of interest policy. Federal regulations require banks to maintain detailed policies to manage such risks. After months of inquiries, Goldman executives provided a series of disjointed documents admitted they did not have a single, firm-wide policy. Segarra determined that the bank's absence of a compliant policy constituted a "Matter Requiring Immediate Attention" (MRIA), a serious regulatory citation that would require board-level intervention. When she presented her findings to her superiors at the New York Fed, she encountered immediate resistance. Her supervisors, including Michael Silva, the senior Fed official at Goldman, pressured her to soften her language and alter her conclusions.

Unbeknownst to her colleagues, Segarra had begun recording her meetings. She captured 46 hours of audio that documented the internal of the New York Fed. The recordings reveal a regulator terrified of upsetting the entity it regulated. In one taped meeting regarding a separate transaction involving the Spanish bank Santander, Silva described a capital relief trade structured by Goldman as "legal shady." The deal appeared designed to help Santander artificially boost its capital ratios, a practice known as "window dressing." even with acknowledging the dubious nature of the transaction, Silva instructed his team not to press the matter, fearing it would damage the Fed's relationship with the bank. He was recorded telling his team, "I don't want to look like we are moving the goalposts."

The conflict over the El Paso deal reached a breaking point in May 2012. Silva summoned Segarra to a meeting and explicitly instructed her to change her finding regarding Goldman's conflict of interest policy. On the recording, Silva is heard telling Segarra, "We have to come off the view that Goldman doesn't have any kind of conflicts of interest policy." He suggested she should instead say the bank had a policy that it needed improvement. Segarra refused, stating that her professional ethics and the evidence prevented her from certifying a policy that did not exist. She told Silva she would not change her conclusion. Three days later, on May 15, 2012, the New York Fed terminated her employment. Security officers escorted her from the building, and her phone and notes were confiscated.

The existence of the tapes remained a secret until September 2014, when ProPublica and This American Life published a detailed investigation. The release of the audio triggered a firestorm in Washington. The recordings provided the public with rare, direct evidence of regulatory capture, confirming the suspicions raised by the Beim Report five years earlier. The Senate Banking Committee convened a hearing in November 2014 to address the allegations. Senator Elizabeth Warren grilled William Dudley, questioning why the Fed had failed to fix the cultural problems identified in 2009. Warren told Dudley, "Is there a cultural problem at the New York Fed? I think the evidence suggests that there is. Either you fix it, Mr. Dudley, or we need to get someone who."

Dudley defended the Fed's actions, claiming that an internal "Operating Committee" had reviewed Segarra's findings and determined that Goldman's policies were sufficient, overruling her. Yet, he offered no concrete evidence to support this claim during the hearing. The testimony did little to quell the public perception that the New York Fed functioned more as a protector of Wall Street than a guardian of the public interest. The revolving door between the regulator and the banks remained a central point of contention; Silva himself had expressed admiration for Goldman executives on the tapes, at one point bragging about how he "fussed at 'em pretty good" to simulate toughness.

Segarra filed a wrongful termination lawsuit against the Federal Reserve Bank of New York, alleging she was fired for refusing to violate the Federal Deposit Insurance Act. In April 2014, U. S. District Judge Ronnie Abrams dismissed the case. The dismissal did not address the truth of Segarra's claims or the content of the tapes. Instead, the ruling relied on a legal technicality: the judge determined that the specific Fed guidance Segarra sought to enforce (SR 08-08) was an advisory letter rather than a statute or regulation. Therefore, her refusal to violate it did not qualify for whistleblower protection under the specific law she. The dismissal was upheld on appeal. The legal system ruled that a bank examiner could be fired for reporting that a bank failed to follow Fed guidance, provided that guidance was not technically a law.

The Carmen Segarra incident remains a defining moment in the history of the Federal Reserve Bank of New York. It exposed the gap between the Fed's public rhetoric of "strong supervision" and the private reality of deference and fear. The tapes demonstrated that even after the catastrophic failures of 2008, the culture of the New York Fed prioritized consensus with banks over the enforcement of safety and soundness. The dismissal of Segarra's lawsuit closed the legal chapter, yet the recordings endure as historical evidence of the structural weaknesses within the American financial regulatory apparatus.

The Bangladesh Bank Heist and Account Security Protocols

On February 4, 2016, the Federal Reserve Bank of New York became the unwitting conduit for one of the most audacious financial crimes in history. Hackers, later identified by the FBI as the North Korean state-sponsored Lazarus Group, targeted the account of the Bangladesh Bank, the central bank of Bangladesh, held at 33 Liberty Street. The attackers did not breach the New York Fed's own firewalls. Instead, they compromised the endpoints in Dhaka, using stolen SWIFT credentials to problem 35 fraudulent payment instructions. These orders directed the New York Fed to transfer nearly $1 billion from the Bangladeshi sovereign account to private entities in the Philippines and Sri Lanka. The event shattered the presumption that central bank-to-central bank transactions were inherently secure.

The mechanics of the heist relied on a deep understanding of the New York Fed's automated processing systems. The hackers timed their attack for a Thursday evening in New York, which corresponded to the start of the weekend in Bangladesh. To mask their activities, they deployed malware that disabled a dot-matrix printer within the Bangladesh Bank's secure room. This printer was designed to produce physical logs of all outgoing SWIFT confirmations. By suppressing these hard copies, the attackers ensured that Dhaka officials would not see the acknowledgment messages sent back by the New York Fed until the banks reopened the following week.

The New York Fed's systems, programmed to trust authenticated SWIFT messages, began processing the requests. Five transactions, totaling $101 million, cleared the initial automated filters. Of this, $20 million was sent to the Shalika Foundation in Sri Lanka, while $81 million was routed to four accounts at the Rizal Commercial Banking Corporation (RCBC) in the Philippines. The remaining 30 transactions, totaling approximately $850 million, were halted. The stoppage occurred not through advanced AI detection, due to a fortuitous coincidence and a spelling error. The hackers misspelled "Foundation" as "Fandation" in the Sri Lankan transfer, prompting a routing bank, Deutsche Bank, to seek clarification. Simultaneously, the reference to the "Jupiter" branch of RCBC in the Philippines triggered a sanctions alert at the New York Fed, as "Jupiter" matched the name of a blacklisted Iranian oil tanker.

The $81 million that successfully left the New York Fed into the Philippine casino sector. The funds were deposited into fictitious accounts at the RCBC branch on Jupiter Street in Makati City, allegedly facilitated by branch manager Maia Deguito. From there, the money was withdrawn, converted into chips at casinos including the Solaire Resort & Casino, and laundered back into the financial system. The speed of the withdrawal exposed a serious latency in the international stop-payment. By the time the Bangladesh Bank re-established contact with the New York Fed after the weekend, the funds were already beyond recall.

The aftermath ignited a diplomatic and legal war over liability. The New York Fed maintained that it followed valid, authenticated instructions and could not be held responsible for the security failures of its account holders. This defense highlighted a widespread vulnerability: the Federal Reserve System is only as secure as the weakest IT department among its foreign account holders. In response, the Fed and SWIFT implemented the Customer Security Programme (CSP), mandating stricter controls for member banks. For a period following the heist, the New York Fed also instituted a "voice verification" protocol for the Bangladesh Bank, requiring telephone confirmation for transfers, a regression to 20th-century methods to ensure 21st-century security.

Litigation over the stolen funds has for a decade. In 2020, Bangladesh Bank filed a civil lawsuit in the New York State Supreme Court against RCBC and several individuals, claiming a massive conspiracy to defraud. RCBC fought to dismiss the case on jurisdictional grounds, arguing the matter belonged in the Philippines. Yet, New York courts have consistently ruled that the use of the correspondent accounts at the New York Fed established the necessary legal nexus. As of early 2026, the case Bangladesh Bank v. Rizal Commercial Banking Corp. remains active in the New York docket, with recent slip opinions addressing procedural motions. While RCBC settled a portion of the claims with a fine to the Philippine central bank, the bulk of the $81 million principal remains unrecovered.

The attribution of the attack to North Korea transformed the heist from a criminal matter into a national security concern. In 2018, the U. S. Department of Justice charged Park Jin Hyok, a programmer linked to the Lazarus Group, alleging the theft was a state-directed operation to bypass sanctions and generate revenue for the regime. The indictment detailed how the attackers spent months inside the Bangladesh Bank network, studying the behavior of bank employees to mimic their keystrokes. This level of espionage demonstrated that the New York Fed's role as the clearinghouse for the global dollar makes it a primary target for rogue states seeking to weaponize the global financial architecture.

Ten years later, the Bangladesh Bank heist remains a definitive case study in the fragility of the global payments system. It forced the New York Fed to reassess its role as a passive processor of sovereign instructions. The bank employs more aggressive anomaly detection algorithms that analyze payment patterns for deviations in size, frequency, and destination. Even with these upgrades, the legal battles in 2026 show that the question of liability, who pays when a sovereign credential is stolen, remains an expensive and unresolved matter of international law.

The September 2019 Repurchase Agreement Market Seizure

| Date | SOFR (Secured) | EFFR (Unsecured) | Fed Target Range |

|---|---|---|---|

| September 16, 2019 | 2. 43% | 2. 25% | 2. 00% , 2. 25% |

| September 17, 2019 | 5. 25% | 2. 30% | 2. 00% , 2. 25% |

| Intraday Peak | 10. 00% | N/A | N/A |

The immediate triggers for this liquidity drought were technical yet predictable. September 16 was the deadline for quarterly corporate tax payments. This pulled roughly $35 billion out of the banking system and into the Treasury General Account. Simultaneously, the settlement of Treasury auctions drained another $54 billion to $100 billion from private sector reserves. These concurrent drains reduced the total pool of reserves in the banking system to approximately $1. 4 trillion. This level was the lowest since 2011. The Federal Reserve had spent years conducting Quantitative Tightening (QT) to shrink its balance sheet. Officials believed $1. 4 trillion represented an "ample" level of reserves. The market proved them wrong. The structural failure lay in the distribution of these reserves. Aggregate data masked a severe scarcity among specific institutions. The largest banks held the vast majority of liquid cash yet refused to lend it into the repo market even as rates hit 10 percent. J. P. Morgan Chase alone held a massive portion of these reserves reduced its discretionary lending to preserve its Liquidity Coverage Ratio (LCR). Regulatory requirements incentivized hoarding rather than intermediation. The system absence a method to redistribute cash from cash-rich banks to cash-starved dealers during stress events. The Open Market Trading Desk at the Federal Reserve Bank of New York reacted with emergency measures. On the morning of September 17, the Desk announced an overnight repo operation to inject up to $75 billion in liquidity. This was the such intervention since the 2008 financial emergency. The operation provided $53. 15 billion to primary dealers. The names of the borrowers, released two years later, revealed that foreign banks and major US dealers were desperate for cash. J. P. Morgan Securities borrowed $7. 6 billion. UBS Securities took $5. 5 billion. BNP Paribas Securities took $5 billion. The Desk continued these daily operations for months to prevent another lockup. This intervention forced the Federal Reserve to reverse its policy of balance sheet reduction. Chairman Jerome Powell insisted the expansion was "not QE" to avoid signaling a change in monetary stance. The data told a different story. Between September 2019 and January 2020, the Federal Reserve bought Treasury bills at a pace that exceeded the asset purchases of QE3. The balance sheet grew by approximately $400 billion in four months. This "organic growth" was necessary to replenish the level of reserves above the $1. 5 trillion threshold that the banking system apparently required to function. The 2019 seizure exposed the danger of operating a "floor system" without a "ceiling." In a floor system, the Fed pays interest on excess reserves (IOER) to keep rates from falling too low. It assumed that ample reserves would naturally prevent rates from spiking too high. The September event proved that without a standing facility to lend cash against collateral, rates could skyrocket without limit. The Federal Reserve Bank of New York had to act as the pawnbroker of last resort. This failure led directly to the establishment of the Standing Repo Facility (SRF) in July 2021. The SRF institutionalized the emergency interventions of 2019. It created a permanent backstop where primary dealers and eligible banks could borrow cash against Treasuries at a penalty rate. This facility capped repo rates and ensured that the volatility of September 2019 would not recur during future tightening pattern. From the vantage point of 2026, the significance of the 2019 repo emergency is clear. It marked the end of the post-emergency experimental phase of balance sheet management. It forced the Federal Reserve to acknowledge that the demand for reserves is not static. The banking system requires a much higher baseline of liquidity due to post-2008 regulations. When the Federal Reserve concluded its subsequent round of balance sheet reduction on December 1, 2025, it did so with the SRF fully operational. The central bank avoided the error of 2019 by maintaining a larger buffer of reserves and ensuring the plumbing had a permanent safety valve. The "repo spike" remains the definitive case study of how regulatory constraints and central bank miscalculations can freeze the most liquid market on Earth.

Pandemic Response and Credit Facility Administration 2020, 2021

In March 2020, the United States Treasury market, the bedrock of the global financial system, ceased to function. Amid the onset of the COVID-19 pandemic, a "dash for cash" triggered a liquidity freeze so severe that the bid-ask spreads on U. S. government debt widened to levels unseen since the 2008 emergency. The Federal Reserve Bank of New York (FRBNY), operating through its Open Market Trading Desk, responded with an intervention that dwarfed all historical precedents. The Desk initially offered $1. 5 trillion -term repurchase agreements (repos) to primary dealers to unfreeze the plumbing of the financial system. This action marked the beginning of a two-year period where the FRBNY nationalized large swathes of the credit risk in the American economy, expanding the Federal Reserve's balance sheet from $4. 2 trillion in early 2020 to nearly $8. 8 trillion by the end of 2021.

The most radical departure from the Federal Reserve's 107-year history occurred on March 23, 2020, when the Board of Governors invoked Section 13(3) of the Federal Reserve Act to establish the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). For the time, the central bank agreed to purchase the debt of private corporations. The FRBNY administered these facilities, which were capitalized by equity from the U. S. Treasury's Exchange Stabilization Fund and later the CARES Act. The stated goal was to stabilize credit markets, yet the execution raised serious questions regarding conflicts of interest and the equitable distribution of liquidity.

To manage these corporate credit facilities, the FRBNY retained BlackRock Financial Markets Advisory as a third-party vendor without a competitive bidding process. The contract gave BlackRock, the world's largest asset manager, the authority to execute trades on behalf of the central bank. In the initial weeks of operation, the SMCCF purchased billions of dollars in exchange-traded funds (ETFs) to provide broad market support. of these purchases flowed directly into BlackRock's own products. By late May 2020, BlackRock's iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) and iShares iBoxx $ High Yield Corporate Bond ETF (HYG) accounted for approximately 48% of the FRBNY's ETF holdings. While BlackRock waived asset management fees on the ETFs the Fed held, the firm continued to collect fees from other investors who poured capital into these funds, following the Fed's signal.

The mere announcement of these facilities achieved the FRBNY's objective before substantial capital was deployed. Credit spreads collapsed, and corporations issued record amounts of debt to build cash buffers. The PMCCF, designed to buy new bond issuances, saw zero usage because private investors, confident in the Fed's backstop, flooded back into the market. The SMCCF peaked at approximately $14. 1 billion in holdings, a fraction of its $250 billion capacity, yet its existence fundamentally altered the perception of risk. The facility also purchased "fallen angels," bonds of companies that held investment-grade ratings as of March 22, 2020, were subsequently downgraded to junk status. This decision socialized the losses of overleveraged corporations, protecting bondholders from the natural consequences of credit downgrades.

In clear contrast to the frictionless support provided to Wall Street and corporate issuers, the Municipal Liquidity Facility (MLF), also administered by the FRBNY, imposed punitive terms on state and local governments. While the corporate facilities bought bonds at market-friendly rates, the MLF charged a penalty premium significantly above normal market yields. Consequently, only two issuers used the facility: the State of Illinois and New York's Metropolitan Transportation Authority (MTA). The MTA, facing a catastrophic drop in ridership, borrowed $2. 9 billion from the MLF when private markets demanded exorbitant yields. The in treatment showed a clear hierarchy in the FRBNY's emergency response: unconditional support for corporate assets and conditional, expensive aid for public entities.

The FRBNY also revived the Term Asset-Backed Securities Loan Facility (TALF), originally designed in 2008. The 2020 version supported the issuance of securities backed by student loans, auto loans, and credit card debt. Unlike the corporate facilities, TALF required investors to put up their own capital, with the Fed providing non-recourse use. This facility saw modest uptake compared to the direct asset purchases, peaking at roughly $4 billion. Simultaneously, the Commercial Paper Funding Facility (CPFF) and Money Market Mutual Fund Liquidity Facility (MMLF) acted as serious backstops, preventing a run on short-term funding markets that corporations use for payroll and inventory.

Throughout 2020 and 2021, the FRBNY's Open Market Trading Desk executed the Federal Open Market Committee's directive to purchase Treasury securities and agency mortgage-backed securities (MBS) at a pace of $120 billion per month. This program, known as Quantitative Easing (QE), continued long after market function had been restored. The relentless buying suppressed interest rates and injected trillions of dollars of reserves into the banking system. Critics this liquidity tsunami decoupled asset prices from economic reality, fueling a speculative mania in equities, housing, and cryptocurrencies while wealth inequality.

The administration of these facilities officially wound down at the end of 2020, with the FRBNY selling its corporate bond portfolio in 2021. The legacy of this period, yet, remains. The FRBNY demonstrated that it possesses the operational capacity to monetize virtually any asset class, from junk bonds to municipal debt. By stepping in to prevent corporate defaults, the central bank created a permanent "Fed Put," signaling to markets that the FRBNY intervene to protect asset values during periods of extreme stress, regardless of the moral hazard it engenders.

| Facility | Capacity | Peak Usage | Asset Class Target | Outcome |

|---|---|---|---|---|

| Secondary Market Corporate Credit Facility (SMCCF) | $250 Billion | ~$14. 1 Billion | Corporate Bonds, ETFs | Compressed spreads; bought BlackRock ETFs and junk bonds. |

| Primary Market Corporate Credit Facility (PMCCF) | $500 Billion | $0 | New Corporate Bond Issuance | Unused; announcement effect restored private lending. |

| Municipal Liquidity Facility (MLF) | $500 Billion | $6. 6 Billion | State & City Debt | High rates limited use to Illinois & NY MTA. |

| Term Asset-Backed Securities Loan Facility (TALF) | $100 Billion | ~$4. 1 Billion | ABS (Auto, Student, Credit Card) | Prevented securitization market freeze. |

| Commercial Paper Funding Facility (CPFF) | Unlimited | ~$4. 3 Billion | Commercial Paper | Backstopped short-term corporate funding. |

Foreign Gold Custody and Repatriation Logistics

Major Sovereign Gold Repatriation Events (2010, 2024)

| Year(s) | Country | Tonnage Removed from NY | Stated Rationale / Context |

|---|---|---|---|

| 2012 | Venezuela | 160 tonnes | President Hugo Chávez ordered repatriation to shield assets from U. S. sanctions. |

| 2013, 2017 | Germany | 300 tonnes | Bundesbank "transparency" initiative; domestic political pressure to verify physical existence. |

| 2014 | Netherlands | 122. 5 tonnes | Dutch Central Bank (DNB) sought to balance storage locations; "public trust." |

| 2017, 2018 | Turkey | 28. 7 tonnes (est.) | Deteriorating U. S.-Turkey relations; Ankara moved reserves to the Bank of England and Istanbul. |

| 2024 | Global (Aggregate) | N/A (Net Outflow) | Continued net outflows as central banks diversify away from U. S. jurisdiction risk. |

The trend of repatriation accelerated following the geopolitical shocks of 2022. When the G7 nations froze the foreign exchange reserves of the Central Bank of Russia, the risk profile of storing gold in New York changed instantly. For decades, the primary risk was theft or invasion;, the primary risk is confiscation by the custodian. Central banks in China, Turkey, and the Middle East took note. While the FRBNY does not publish a live country-by-country breakdown of holdings, the aggregate weight in the vault has declined from its 1973 peak of over 12, 000 tons to roughly half that amount today. The mechanics of repatriation involve heavy security transport. Armored carriers, frequently coordinated by the Bank for International Settlements (BIS) or private security firms, transport the bullion from 33 Liberty Street to nearby airports. From there, the metal flies on cargo aircraft to the destination country. The cost of these operations is substantial. Germany's repatriation program cost approximately €7. 7 million, covering transport, insurance, and recasting. even with the outflows, the New York Fed remains a serious node in the global gold market. It allows nations to settle balance-of-payments deficits without physical shipment. If Country A owes Country B money, and both hold gold at the Fed, they can simply instruct the Fed to move bars from Compartment A to Compartment B. The Fed charges a nominal fee of $1. 26 per bar for this internal book-entry transfer. This efficiency keeps nations tethered to the vault, even as trust in the geopolitical neutrality of the U. S. financial system. The physical reality of the vault, bedrock, steel, and armed guards, remains static, the ownership map inside the cages is shifting rapidly away from the West.

Balance Sheet Reduction and Regional Bank Oversight 2022, 2026

In June 2022, the Open Market Trading Desk at 33 Liberty Street initiated the most aggressive financial contraction in the history of the Federal Reserve Bank of New York. After swelling the System Open Market Account (SOMA) to nearly $9 trillion during the pandemic response, the New York Fed began the mechanical process of Quantitative Tightening (QT). This reversal required the Desk to stop reinvesting principal payments from maturing Treasuries and mortgage-backed securities (MBS), destroying liquidity at a capped rate of $95 billion per month. By February 2026, this operation had drained approximately $2. 4 trillion from the financial system, reducing the balance sheet to $6. 6 trillion. While this reduction successfully tightened financial conditions, it inflicted catastrophic damage on the New York Fed's own income statement, creating a zombie accounting entry that haunt the central bank for a decade.

The mechanics of this financial self-immolation were simple devastating. To control interest rates, the Federal Reserve pays commercial banks interest on the reserves they park at the Fed. As the Federal Open Market Committee (FOMC) hiked rates from near-zero to over 5% in 2023, the New York Fed's interest expense skyrocketed. Simultaneously, the income generated by the SOMA portfolio remained stagnant, locked into the low-yielding 2% bonds purchased during the Quantitative Easing (QE) era. The result was a negative spread that bled billions of dollars monthly. In 2023, the Federal Reserve System reported an operating loss of $114. 3 billion, followed by a $77. 6 billion loss in 2024. Under standard accounting rules, a private bank facing such losses would be insolvent. The Federal Reserve, yet, uses a unique accounting device known as a "deferred asset." Rather than deducting losses from its capital, the Fed records them as a negative liability, a pledge to pay the U. S. Treasury from future earnings. By early 2026, this deferred asset had ballooned to nearly $242 billion, ending the Fed's remittances to the taxpayer for years to come.

While the New York Fed struggled with its own balance sheet, its supervision of regional bank holding companies collapsed in real-time. The failure of Signature Bank in March 2023 exposed a dangerous gap in regulatory enforcement. Although the FDIC served as Signature's primary federal regulator, the bank's collapse triggered a widespread panic that forced the New York Fed to open its Discount Window and administer the emergency Bank Term Funding Program (BTFP). The BTFP allowed banks to pledge underwater bonds at par value, a temporary suspension of market reality that injected billions into the New York banking sector. This intervention prevented immediate contagion did nothing to cure the underlying rot in commercial real estate (CRE) portfolios, a sector heavily concentrated on the books of New York regional lenders.

The consequences of this oversight negligence materialized in January 2024 with the near-collapse of New York Community Bancorp (NYCB). As the holding company regulator, the Federal Reserve had approved NYCB's acquisition of Flagstar Bank in late 2022 and its purchase of Signature Bank's assets in 2023. These approvals allowed NYCB to cross the $100 billion asset threshold, subjecting it to stricter capital requirements it was unprepared to meet. In early 2024, NYCB shocked markets by reporting a $2. 4 billion impairment charge and "material weaknesses" in its internal loan review controls. The stock plummeted, dragging the entire regional banking index down with it. The debacle revealed that New York Fed examiners had allowed a rapid consolidation of assets under a management team absence the risk controls to handle them. The "material weakness" was not a sudden accident; it was a festering governance failure that supervisors missed during the merger approval process.

By 2025, the commercial real estate emergency in New York City had become the primary drag on regional bank stability. High interest rates, driven by the Fed's own policy, decimated the valuations of rent-stabilized multifamily units and office towers. Regional banks, which held the majority of these loans, faced a slow-motion insolvency. The New York Fed's supervision teams responded by demanding higher capital buffers, forcing banks to sell assets at deep discounts or seek dilutive private equity lifelines. The "soft landing" touted by economists did not apply to the balance sheets of community lenders, who remained trapped between the Fed's high rate floor and the collapsing value of their collateral.

As of February 2026, the Federal Reserve Bank of New York operates in a state of suspended financial animation. The Reverse Repo (RRP) facility, which once absorbed over $2. 5 trillion in excess cash, sits nearly empty, its balances drained to under $1 billion to fund the Treasury's issuance. The balance sheet reduction formally concluded in October 2025, leaving the system with "ample" not "abundant" reserves. Yet, the legacy of the 2022, 2026 period remains visible on the ledger. The $242 billion deferred asset represents a massive transfer of wealth from the public purse to the commercial banking sector, as the Fed continues to pay high interest on reserves while generating nothing for the Treasury. The central bank successfully defended the currency, in doing so, it broke the regional banking model and rendered itself technically insolvent.

| Metric | 2021 (QE Peak) | 2023 (Loss Era) | 2024 (Stabilization) | 2026 (Current Status) |

|---|---|---|---|---|

| Total Assets | $8. 8 Trillion | $7. 7 Trillion | $7. 0 Trillion | $6. 6 Trillion |

| Net Income/Loss | +$107. 9 Billion | -$114. 3 Billion | -$77. 6 Billion | -$25. 0 Billion (Est) |

| Remittances to Treasury | $109. 0 Billion | $0 | $0 | $0 |

| Deferred Asset Size | $0 | $133. 0 Billion | $211. 0 Billion | $242. 0 Billion |

| Reverse Repo Usage | $1. 6 Trillion | $2. 2 Trillion | $600 Billion | $0. 9 Billion |